As harvest was in full swing, farmers across the U.S. were faced with high input costs, lower crop production and uncertainty as policy changes loomed on the horizon throughout the months of September and October.

It is necessary for not only farmers, but also seed experts, to be aware of challenges across the world that will inevitably impact the crop and to gear themselves with knowledge to help along the way.

Here are the agricultural highlights for the months of September and October 2022.

Crop Production

The global cereal production is pegged at 2,768 million tons, hitting 1.7% below 2021’s numbers, while the world coarse grain output is predicted to meet 1,468 tons, falling 2.8% year-on-year. The U.S. wheat ending stocks are forecast down for 2022/23, settling at 576 million bushels in October. This outcome is the smallest in 15 years. U.S. wheat crop is down 133 million form September, now predicted to be 1.650 billion bushels, making these numbers the second lowest in 20 years. Future prices have soared in recent weeks, responding to tight U.S. supplies and uncertainty across the globe about Black Sea wheat shipments.

Corn and soybean production continued to fall when compared to 2021 numbers, according to the USDA’s National Agricultural Statistics Service (NASS) Oct. 11 Crop Production report.

As of Oct. 1, conditions showed that soybean yields ring in at 49.8 bushels per acre, falling 1.9 bushels from 2021. On the flip side, area harvested for soybeans is projected at 86.6 million acres, a slight increase from 2021.

While corn production was forecasted at 14.4 billion bushels in the USDA’s August Crop Production report, it dropped to 13.9 billion bushels in October. This means that corn production has now fallen 8% from 2021. Corn yields were predicted to average 171.9 bushels for each acre harvested, falling 4.8 bushels since 2021.

Despite harsh weather conditions with high temperatures and a lack of rainfall, the real culprit of the downturn in corn this year is due to corn’s input costs and inflation, experts believe.

“What drove that shift in corn acreage and soybean acreage here in Indiana was almost exclusively economics,” says Bob Nielsen, Purdue University Extension corn specialist and professor of agronomy, noting that grain prices — while exceptional for both corn and soybeans — were slightly more in favor of soybeans this year.

“More importantly, there was a run up in input costs for corn compared to soybeans prior to the beginning of the season,” Nielsen adds. “That led a lot of people to shift more acres into soybeans and fewer to corn as a response to those high inputs.”

Fertilizer and Commodity Prices

High fertilizer prices are just another piece of the puzzle that have created obstacles for farmers throughout the season.

According to the Agricultural Marketing Service, fertilizer prices on July 14 were $1,469 per ton for anhydrous ammonia, $983 per ton for diammonium phosphate (DAP), and $862 per ton for potash. Adding to that, according to University of Illinois’s Nitrogen Fertilizer Outlook for 2023 Decisions, the report states all of those prices were increased in comparison to the previous year — anhydrous ammonia prices have increased from $726 per ton on July 15, 2021, an increase of $743 per ton. DAP has increased from $688 per ton, an increase of $295 per ton. Potash has risen from $481 per ton, an increase of $381.

Based on these numbers, experts believe that fertilizer prices will remain high, causing great expenses for farmers in 2023. Due to limited supplies and increased prices, the predicted season-average farm price — which was already record high — hit $9.20, increasing $0.20.

In good news, the world food commodity prices once again declined, making September the sixth consecutive month to see a decrease. The Food and Agriculture Organization of the United Nations’ (FAO) Food Price Index averaged 136.6 points during September, falling 1.1% from August, yet remaining 5.5% higher than the same time last year.

The steep decline in vegetable oil quotations are to thank, with those cheaper prices offsetting higher cereal prices, according to FAO. Vegetable oil decreased by 6.6%, reaching the lowest level its seen since February 2021. Palm, soy, sunflower and rapeseed oils’ international quotations were collectively lower. In contrast, the FAO Cereal Price Index increased 1.5% from August to September.

Farmer Sentiment

Despite some decrease in commodity prices, high fertilizer prices remain top of mind for U.S. producers, largely contributing to the fall in farmer sentiment.

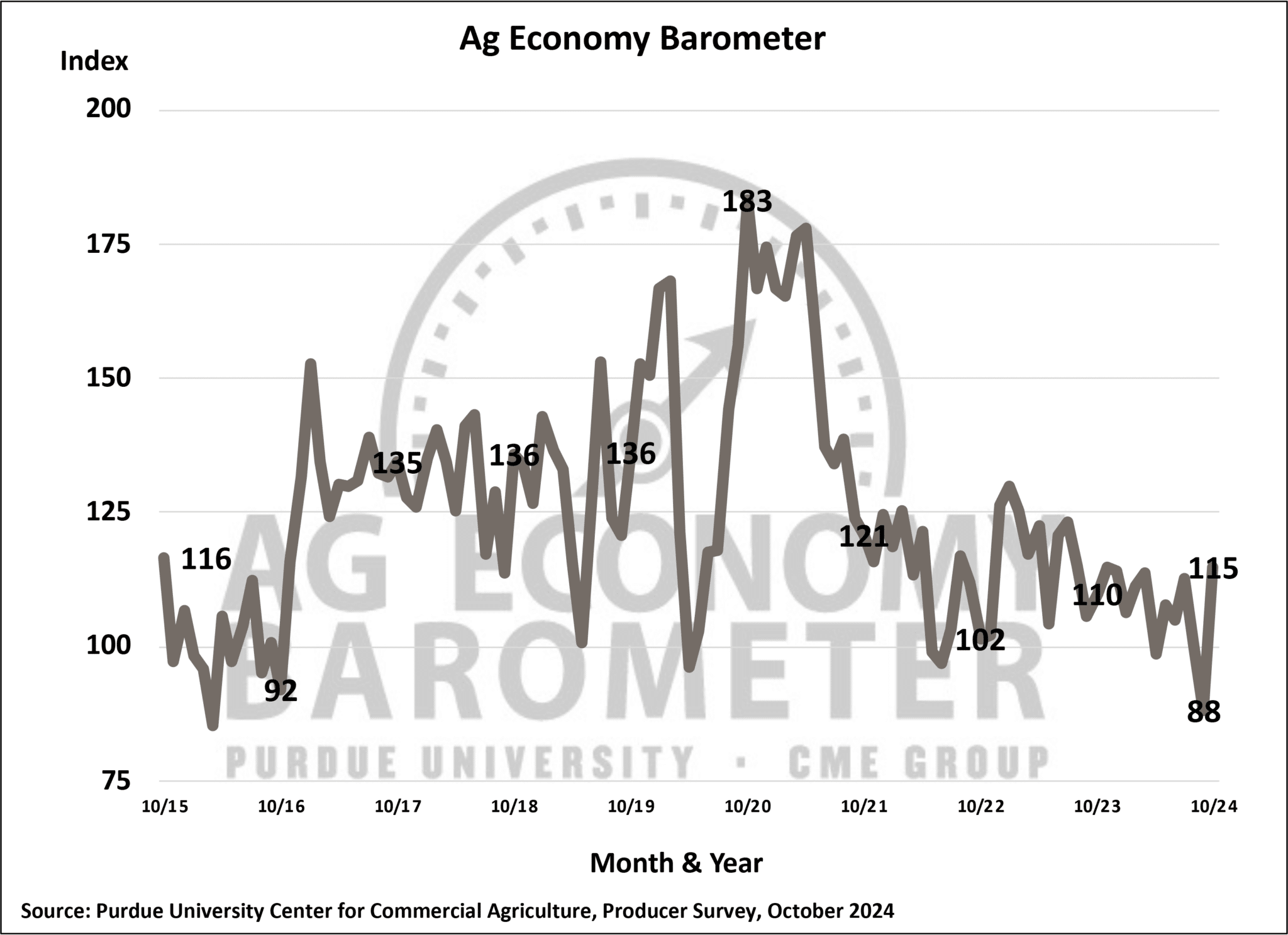

In fact, the Purdue University-CME Group Ag Economy Barometer sentiment index found that 44% of participants chose “higher input costs” when asked their number one concern — yet it is important to note that percentage is less than August’s result of 53%. “Rising interest rates” was second on the list for producer concerns, chosen by 23% participants. “Availability of inputs” came third, chosen by 14% of participants.

The index fell 5 points from August to September, drifting lower to 112. Compared to 2021, the barometer in September was 10% lower and producers’ assessment of current conditions in the Current Conditions Index fell 22%.

Midterm Elections

As November’s Midterm elections approached, farmer’s had various factors to consider — one being, why are Midterm elections so crucial for the agriculture industry? While this could mean change for the U.S. in terms of policy and regulations, it also could have ramifications for the agriculture industry — particularly the 2023 Farm Bill.

The bill is up for reauthorization next year and includes all the USDA’s major programs such as nutrition, farm programs, conservation, trade and research. The last Farm Bill cost $867 billion. While funding from the bill is essential to reach goals in the industry, oftentimes it is difficult to convince officials in Washington D.C. that American growers need the money, making the officials elected in Midterms crucial to the future of the industry.

Therefore, September and October left farmers with a multitude of uncertainties about the future on farm and in the U.S.

Related Articles:

As Summer Comes to a Close, Farmers Face Drought and Production Challenges

Farmer Highlights: May and June